Transition vers une fiscalité simplifiée ou constitution d'une personne morale.

Pour comptabiliser les revenus et les dépenses des entrepreneurs individuels, vous pouvez utiliser des fournitures spéciales de la version de base de « 1C : Comptabilité 8 »* : « 1C : Entrepreneur 8 » et « 1C : Simplifié 8 ». S.A. explique comment les configurer pour la tenue des dossiers. Kharitonov, docteur en économie, professeur à l'Académie financière du gouvernement de la Fédération de Russie.

Note:

"1C:Entrepreneur 8"

"1C : 8 simplifié"

- Impôt sur le revenu d'un entrepreneur

- fiscalité simplifiée

Entreprise ->

A propos des possibilités de « 1C : Comptabilité 8 » pour les entrepreneurs individuels

Note:

* Veuillez noter que 1C fournit une assistance gratuite pour les versions de base des produits logiciels 1C:Enterprise 8.

Les particuliers peuvent exercer des activités entrepreneuriales sans constituer une personne morale. Pour ce faire, ils doivent s'inscrire de la manière prescrite en tant qu'entrepreneurs individuels. Dès leur enregistrement auprès de l'État, les entrepreneurs individuels deviennent des entités commerciales et sont tenus de payer des impôts sur les revenus perçus dans le cadre de leurs activités commerciales. La procédure d'imposition de ces revenus dépend du régime fiscal applicable. Il peut y avoir plusieurs options conformément au Code des impôts de la Fédération de Russie :

- paiement de l'UTII pour certains types d'activités conformément au chapitre 26.3 du Code des impôts de la Fédération de Russie ;

- application d'un système fiscal simplifié conformément au chapitre 26.3 du Code des impôts de la Fédération de Russie ;

- paiement de l'impôt sur le revenu des personnes physiques conformément au chapitre 23 du Code des impôts de la Fédération de Russie (ci-après dénommé le régime fiscal général). Si les entrepreneurs individuels n'appliquent pas de régimes fiscaux spéciaux, ils sont alors reconnus comme contribuables pour leurs activités commerciales sur la base du chapitre 23 « Impôt sur le revenu des particuliers » du Code des impôts de la Fédération de Russie (ci-après dénommé le « régime fiscal général ». »).

Dans ce dernier cas, le calcul de l'assiette fiscale à la fin de chaque période fiscale est effectué sur la base des données comptables des revenus, dépenses et transactions commerciales de la manière déterminée par le ministère des Finances de la Russie (clause 2 de l'article 54 du Code des impôts de la Fédération de Russie).

La procédure actuelle de comptabilisation des revenus, des dépenses et des transactions commerciales des entrepreneurs individuels a été approuvée par un arrêté conjoint du ministère des Finances de la Russie et du ministère des Impôts de la Russie du 13 août 2002 n° 86n/BG-3-04/. 430. Il prévoit que la comptabilisation des transactions sur les revenus perçus et les dépenses engagées est effectuée par les entrepreneurs individuels en enregistrant dans le Livre de comptabilité des revenus et dépenses et des opérations commerciales d'un entrepreneur individuel (ci-après dénommé KUDiR) les transactions concernant les revenus reçus et les dépenses engagées. . Les entrées dans KUDiR sont effectuées de manière positionnelle au moment des transactions sur la base de documents primaires.

KUDiR se compose de six sections, dont plus de vingt tableaux. Remplir chaque tableau et résumer les données pour calculer l'assiette fiscale est une tâche non triviale et nécessite que l'entrepreneur individuel ait de très bonnes connaissances non seulement dans le domaine de la fiscalité, mais aussi de la comptabilité.

Pour que la maintenance de KUDiR ne devienne pas « l'objectif principal » de l'activité commerciale, il est nécessaire d'automatiser la comptabilité. "1C : Comptabilité 8" prend en charge la comptabilité de différents régimes fiscaux, incl. et le paiement de l'impôt sur le revenu des personnes physiques par les entrepreneurs individuels. Pour faciliter la prise en main de la comptabilité, une livraison spéciale « 1C : Comptabilité 8 » a été publiée "1C:Entrepreneur 8". Il vous permet d'automatiser la comptabilité des revenus et dépenses et des transactions commerciales des entrepreneurs individuels et de générer automatiquement du KUDiR conformément à la procédure établie. De plus, le programme vous permet d'automatiser les calculs d'un certain nombre d'impôts dont le payeur est un entrepreneur individuel, notamment la TVA, l'impôt unifié, etc.

Parallèlement, en cas de transition vers l'utilisation d'une fiscalité simplifiée pour un entrepreneur individuel utilisant la livraison spéciale « 1C : Entrepreneur 8 », il n'est pas nécessaire de changer de programme comptable, il suffit de modifier les paramètres. Et ceci malgré le fait que pour les organisations et les entrepreneurs utilisant le régime fiscal simplifié, 1C a publié une autre livraison spéciale « 1C : Comptabilité 8 » - "1C : 8 simplifié". Le fait est que les deux livraisons spéciales (« 1C : Entrepreneur 8 » et « 1C : Simplifié 8 ») sont une version spécialement préconfigurée de la version de base de la configuration « Enterprise Accounting ». Ils diffèrent les uns des autres et de « 1C : Comptabilité 8 » par leurs bases de démonstration et par le fait que les développeurs ont initialement configuré chaque programme de manière à simplifier au maximum la comptabilité des activités de l'entreprise, en fonction du régime fiscal utilisé, rendre le travail transparent, compréhensible et efficace. Deux interfaces spéciales ont été créées à cet effet :

- Impôt sur le revenu d'un entrepreneur(l'interface principale du programme "1C:Entrepreneur 8");

- fiscalité simplifiée(l'interface principale du programme "1C : Simplifié 8").

Dans chaque interface, les développeurs n'ont inclus que les objets nécessaires à la tenue de registres des activités commerciales d'un entrepreneur individuel et ont organisé le travail avec eux de manière à ne demander que les informations directement et directement liées à la fiscalité correspondante. régime.

La transition d'un programme à un autre est très simple - juste sous une forme spéciale ouverte par la commande de menu Entreprise -> Régimes fiscaux applicables, modifiez le système de taxation appliqué et précisez les paramètres de la nouvelle politique comptable ou modifiez l'interface.

Pour les entrepreneurs assujettis à un impôt unique sur les revenus imputés pour certains types d'activités (UTII), il est possible de tenir des registres séparés des transactions commerciales par types d'activités soumises à l'impôt sur le revenu des personnes physiques (ou fiscalité simplifiée) et à l'UTII.

Les deux livraisons spéciales de « 1C : Comptabilité 8 » (« 1C : Entrepreneur 8 » et « 1C : Simplifié 8 ») proposent une telle comptabilité en personnalisant en outre leurs paramètres. Ce paramétrage peut être effectué aussi bien pendant la période d'application du régime général de taxation que pendant la période d'application du régime fiscal simplifié.

À propos des paramètres de stratégie comptable

« 1C : Entrepreneur 8 » et « 1C : Simplifié 8 » sont des produits logiciels personnalisables, c'est-à-dire qu'ils offrent la possibilité de contrôler le comportement du programme lors de l'inscription dans la base d'informations des transactions commerciales, en fonction des paramètres de politique comptable.

Concernant le terme « politique comptable », nous notons qu'en relation avec la configuration « Enterprise Accounting », la politique comptable désigne un ensemble de paramètres qui contrôlent le comportement du programme. Les paramètres de politique comptable sont le système fiscal, la nature de l'activité d'un entrepreneur individuel, le principal type d'activité, etc.

Les paramètres de politique comptable sont stockés dans le programme dans le registre d'informations Politiques comptables des organisations(menu Entreprise -> Politique comptable -> Politique comptable des organisations). Considérons-les par rapport à une livraison spéciale "1C:Entrepreneur 8".

La première inscription dans ce registre est généralement effectuée lorsque vous travaillez avec l'assistant de démarrage lors du remplissage du formulaire. Politique comptable(voir fig. 1).

Riz. 1

En remplissant ce formulaire dans la section Activité principale il faut préciser Nature principale de l'activité entrepreneur individuel et Groupe principal de nomenclature.

La nature principale de l'activité est indiquée dans les détails Nature de l'activité en sélectionnant une valeur dans la liste proposée :

- De gros;

- Vente au détail;

- Commerce de détail soumis à l'UTII ;

- Production (travaux, services) ;

- Prestations soumises à l'UTII.

Le groupe principal de la nomenclature est indiqué dans les détails comme une chaîne de caractères. Ces informations sont inscrites dans l'annuaire Groupes de nomenclature.

Si, selon le certificat d'enregistrement d'État, un entrepreneur individuel envisage d'exercer plusieurs types d'activités, alors . Nous nous attarderons plus tard sur les caractéristiques d'un ajustement supplémentaire des paramètres de politique comptable dans ce cas.

Si un ou plusieurs types d'activités commerciales sont transférés à l'UTII, alors pour activer un mécanisme de comptabilisation séparée des revenus et des dépenses dans la section Comptabilité fiscale la case doit être cochée L'organisme est assujetti à l'impôt unique sur les revenus imputés (UTII).

Sous le régime fiscal général, un entrepreneur individuel est reconnu comme contribuable à la taxe sur la valeur ajoutée. Si, en plus des opérations de vente imposées au taux de 18 % (et/ou 10 %), un entrepreneur individuel envisage de réaliser des opérations de vente non soumises à la TVA et/ou imposées au taux de 0 %, alors en section Comptabilité fiscale la case doit être cochée .

En raison du fait qu'à partir du 1er janvier 2008, une période fiscale trimestrielle unique a été établie pour tous les contribuables à la TVA (article 163 du Code des impôts de la Fédération de Russie tel que modifié par la loi fédérale n° 137-FZ du 27 juillet 2006), détails Période d'imposition pour la TVA ne peut pas être modifié.

En fait, l'ensemble des paramètres de politique comptable ne se limite pas à ceux que l'assistant de démarrage propose de préciser. Pour les autres paramètres, le programme définit automatiquement les valeurs par défaut. Peut-être que ces valeurs conviennent à l'entrepreneur individuel, mais peut-être pas. A cet égard, lors de la maîtrise du programme, il est recommandé d'ouvrir le formulaire d'inscription et d'analyser les paramètres définis.

Tous les paramètres de méthodes comptables sont divisés en groupes en fonction de leur objectif. Les paramètres de chaque groupe sont résumés sur des onglets séparés.

Options comptables

En particulier, sur les onglets Comptabilité Et Production Les paramètres qui contrôlent le comportement du sous-système comptable sont placés.

Oui, sur l'onglet Comptabilité sont indiqués (voir Fig. 2) :

- méthode d'évaluation des biens destinés à la vente au détail (valeurs possibles Par prix d'achat(par défaut) ou Par prix de vente);

- la procédure d'annulation des dépenses du compte 26 « Frais généraux d'entreprise » (par défaut, les dépenses de fin de mois sont transférées du compte 26 « Frais généraux d'entreprise » au compte 20 « Production principale »).

Riz. 2

Le troisième paramètre de cet onglet précise la méthode de valorisation des stocks dans l'entrepôt. Lors de la tenue des registres des dépenses d'un entrepreneur individuel, une seule méthode est possible - FIFO*, les détails ne peuvent donc pas être modifiés.

Note:

* Une méthode d'évaluation des matériaux, dans laquelle, quel que soit le lot de matériaux mis en production, les matériaux sont d'abord amortis au prix du premier lot acheté, du second, etc. par ordre de priorité, jusqu'à la consommation totale de matières est obtenu (ndlr) .

Paramètres de comptabilité des coûts de production

Sur l'onglet Production les paramètres de comptabilisation des coûts de production sont indiqués. Ils sont utilisés si l'activité commerciale est liée à la production de produits, à l'exécution de travaux ou à la fourniture de services.

Sur un sous-onglet Comptes 20.23 indique l'ordre que le programme doit suivre lors de la répartition des coûts de production principale et auxiliaire (voir Fig. 3).

Riz. 3

Par défaut, le programme répartit ces dépenses selon les règles suivantes :

- coûts de production - . Il n’y a pas d’alternative ;

- dépenses pour la fourniture de services à des clients tiers - Basé sur les coûts de production et les revenus prévus. Options alternatives : Par coût de production prévu, Par chiffre d'affaires;

- dépenses pour la fourniture de services à ses propres divisions - Au coût de production prévu. Options alternatives : Par volume de production, par coût de production prévu et volume de production.

Sur un sous-onglet Comptes 25, 26 le mode de répartition des frais généraux de production, ainsi que des frais généraux d'exploitation, est indiqué s'ils sont amortis sur le compte 20 « Production principale ».

Selon les spécificités de l'activité de production exercée par un entrepreneur individuel, différentes bases de répartition peuvent être utilisées lors de la répartition de la production générale et des frais généraux d'entreprise.

L'assiette de répartition des coûts est fixée dans le registre d'information Méthodes de répartition des coûts indirects des organisations dans la colonne Base de distribution.

La distribution peut être effectuée en utilisant l'une des méthodes suivantes :

- Volume d'émission- la quantité de produits fabriqués dans le mois en cours et de services fournis est utilisée comme base de distribution ;

- Coût prévu- le coût prévu des produits sortis dans le mois en cours et des services fournis est utilisé comme base de distribution ;

- Rémunération- le montant des dépenses reflété dans les postes de coûts de type est utilisé comme base de répartition Rémunération;

- Coûts du matériel- le montant des dépenses reflété dans les éléments de type Coûts du matériel;

- Revenu- le montant du chiffre d'affaires de chaque groupe de produits est utilisé comme base de distribution ;

- Coûts directs- les données sur le montant des coûts directs pour chaque groupe de produits sont utilisées comme base de répartition ;

- Éléments de coûts directs sélectionnés- les données sur des éléments de coûts directs spécifiques sont utilisées comme base de répartition (les éléments de coûts sont indiqués dans la colonne Liste des éléments de coûts).

La méthode de répartition peut être définie avec une précision de la division et du poste de coût. Cela peut être nécessaire lorsque différents types de dépenses nécessitent des méthodes de répartition différentes.

S'il est nécessaire d'établir une méthode de répartition générale pour toutes les dépenses générales et générales de production, alors lors de la définition de la méthode de répartition, vous n'avez pas besoin de spécifier le compte de coûts, la division et le poste de coût. De même, un mode de répartition générale est établi pour toutes les dépenses comptabilisées dans un seul compte ou dans une seule division.

Lors de l'établissement d'un mode de répartition, la date à partir de laquelle il est appliqué est indiquée. Si le mode établi doit être modifié, une nouvelle inscription est inscrite au registre indiquant le nouveau mode de répartition et la date à partir de laquelle le nouveau mode doit être appliqué.

Le programme « 1C:Entrepreneur 8 » prend en charge deux méthodes de comptabilisation des produits finis (travaux, services) : avec et sans utilisation du compte 40 « Sortie de produits (travaux, services) ». Dans la première méthode, on suppose que la production de produits (travaux, services) au cours du mois est estimée au coût prévu.

En comptabilité, la libération se traduit par une écriture du crédit du compte 40 au débit du compte 43 « Produits finis » (au débit du compte 90.02 « Coût des ventes » - pour travaux, services). A la fin du mois, les coûts réels de production sont passés du crédit du compte 20 au débit du compte 40, et le coût réel des produits vendus (travaux, services) est ajusté du montant de la différence.

Avec la deuxième méthode, les coûts réels sont radiés du compte 20, en contournant le compte 40.

Le mode de comptabilisation de l'émission est indiqué sur le sous-onglet Sortie de produits et services. Par défaut, on considère que la comptabilité est tenue Sans utiliser le compte 40. Mais si l’organisation décide d’évaluer la production au coût prévu, la valeur de la méthode doit être modifiée.

Si un entrepreneur individuel est engagé dans la production de produits multi-productions, alors sur le sous-onglet Redistribution il est nécessaire d'indiquer l'ordre des répartitions (voir Fig. 4). Parallèlement, dans le registre d'information Contre-production de produits (services) et radiation de produits pour propres besoins décrit les règles de clôture des comptes de frais.

Riz. 4

Saisie des informations sur les dépenses comptables par type d'activité

Sur l'onglet Entrepreneur les paramètres du principal type d'activité de l'entrepreneur individuel sont indiqués, ainsi que des informations sur les types d'activités exercées (voir Fig. 5).

Riz. 5

La nature principale de l'activité (la valeur des accessoires Nature de l'activité) et le groupe de nomenclature principal (la valeur de l'attribut Groupe de nomenclature (type de biens, travaux, services)) sont utilisés comme valeurs par défaut lors de la réflexion des transactions de réception de biens (travaux, services) dans la base d'informations, si au moment de la saisie des données on ne sait pas à quel type d'activité se rapporte cette réception.

Si un entrepreneur individuel exerce plusieurs types d'activités, cochez la case Un entrepreneur tient des registres de plusieurs types d’activités., et dans le répertoire Types d'activités des entrepreneurs décrire tous les types d'activités (y compris celle indiquée comme principale).

Paramètres comptables pour les calculs de TVA

Sur l'onglet T.V.A. spécifie les paramètres de comptabilisation des calculs de taxe sur la valeur ajoutée.

Le programme prend en charge deux options de comptabilité de la TVA, classiquement appelées « régulière » et « simplifiée ».

Dans la première option, des documents spéciaux du sous-système de comptabilité TVA sont utilisés pour déterminer les montants des déductions fiscales.

La deuxième option consiste à accepter la TVA « en amont » en déduction immédiatement lors de l'enregistrement de la facture du fournisseur lors de la comptabilisation des documents à l'aide desquels la réception des biens (travaux, services) est reflétée dans la base d'informations. La deuxième option demande moins de main-d'œuvre, mais elle est recommandée lorsqu'un entrepreneur individuel exerce des activités qui ne présentent aucune caractéristique fiscale. En particulier, si certains types d'activités d'un entrepreneur individuel ne sont pas transférés au paiement de l'UTII, l'entrepreneur individuel ne réalise pas de construction de capital, etc. Cependant, si de telles caractéristiques surviennent, le programme permet de les prendre en compte, mais manuellement.

Par défaut, le programme applique la première option de comptabilité TVA. Pour passer au second dans les paramètres de politique comptable, vous devez cocher la case Comptabilité TVA simplifiée.

Actuellement, l'assiette fiscale des opérations de vente est déterminée « par expédition », donc la valeur de l'attribut Moment de détermination de l'assiette fiscale sur un sous-onglet Comptabilité TVA non disponible pour le changement.

Il y a deux autres cases à cocher sur l'onglet. Objectif de la case à cocher L'organisation réalise des ventes sans TVA ou avec TVA 0% nous avons expliqué ci-dessus.

Par rapport à la deuxième case à cocher Facturer la TVA sur l'expédition sans transfert de propriété Notons ce qui suit. Après que la loi fédérale n° 119-FZ du 22 juillet 2005 a modifié les articles 166 et 167 du Code des impôts de la Fédération de Russie, deux points de vue ont émergé sur la question du calcul de la TVA sur les opérations de transfert de biens à vendre. Selon la première, exprimée officieusement par des représentants de l'administration fiscale, l'assiette fiscale doit être déterminée au moment de l'expédition des marchandises au commissionnaire. Selon la seconde, actuellement suivie par la plupart des spécialistes, lors de l'expédition de marchandises à un commissionnaire, il n'y a aucune raison de facturer la TVA, puisqu'il n'y a pas d'objet de taxation - l'opération de vente proprement dite. En lien avec ce qui précède, l'indicateur de calcul de la TVA sur les opérations d'expédition de marchandises sans transfert de propriété n'est pas paramétré par défaut.

Si la comptabilité TVA est effectuée de la manière « habituelle », alors sur le sous-onglet Comptabilisation des règlements une stratégie peut être spécifiée pour déterminer le montant des taxes en amont et en sortie dans des situations complexes (voir Figure 6). Par rapport à la TVA « en amont », nous entendons des situations où une partie du montant de la taxe peut être déduite, mais une partie ne le peut pas (par exemple, les dépenses concernent des opérations non soumises à la TVA). Par défaut, le programme considérera en premier les valeurs sur lesquelles la TVA est payée. ne peut pas être déduit. Par rapport à la TVA « en aval », nous entendons les situations où les opérations de vente sont taxées, y compris au taux de 0 %. Par défaut, on considère que les biens (travaux, services) vendus au taux de TVA 0% sont payés en dernier.

Riz. 6

Sur un sous-onglet Différences de montant Un seul détail est disponible pour modification, dans lequel, à l'aide de la case à cocher, vous pouvez définir le mode dans lequel le programme générera des factures pour les calculs en unités conventionnelles en roubles. Par défaut, ce mode (case à cocher) n'est pas sélectionné.

Paramètre de comptabilité fiscale des revenus et dépenses selon le régime fiscal simplifié

Si un entrepreneur individuel qui exerce déjà des activités commerciales sous le régime fiscal général décide de passer au régime fiscal simplifié, le registre Politiques comptables des organisations une nouvelle entrée doit être saisie. Dans cette entrée, vous devez indiquer à quelle période elle se rapporte, changer le régime fiscal en Simplifié, remplissez les onglets du régime fiscal simplifié et des assurances sociales (si une décision est prise de payer volontairement des cotisations à la Caisse d'assurance sociale de la Fédération de Russie).

La procédure de remplissage de ces onglets pour un entrepreneur individuel ne diffère pas de la procédure de remplissage par les organisations*.

Paramètres de comptabilité fiscale pour l'UTII

Si un entrepreneur individuel pour certains types d'activités est transféré au paiement de l'UTII, alors, selon la date à laquelle un tel transfert a eu lieu, soit sous la forme d'une écriture sur les politiques comptables de l'année suivante, soit dans une écriture complémentaire datée du début du trimestre correspondant, vous devez cocher la case UTII pour certains types d'activités et remplissez l'onglet UTII.

Si un entrepreneur individuel appliquant le régime général de fiscalité est transféré au paiement de l'UTII, alors sur cet onglet vous devez indiquer :

- si un entrepreneur individuel est reconnu comme payeur de l'UTII pour le commerce de détail. Par défaut, on considère qu'il est reconnu (le flag est positionné Le commerce de détail est soumis à un impôt unique sur le revenu imputé);

- ou Pendant un mois(valeur par défaut) ;

- Revenus des ventes(par défaut) ou Produits des ventes et hors exploitation.

Si un entrepreneur individuel appliquant une fiscalité simplifiée est transféré pour payer l'UTII pour certains types d'activités, alors sur l'onglet UTII vous devez indiquer (voir Fig. 7) :

- si un entrepreneur individuel est reconnu comme payeur UTII pour le commerce de détail (reconnu par défaut) ;

- quelle méthode est utilisée pour répartir les dépenses qui ne peuvent être directement imputées aux activités soumises à l'UTII - Pour le trimestre(par défaut) ou Total cumulé depuis le début de l'année;

- ce qui sert de base à la répartition de ces dépenses : Revenu des ventes (SA), Revenu total (NU) ou Revenu accepté (NU).

Riz. 7

Pour la méthode de distribution Revenu total (NU) la somme de tous les revenus d'un entrepreneur individuel, déterminé par la méthode de trésorerie, est utilisée comme base - c'est la valeur de l'indicateur Revenu - total KUDiR (nous vous rappelons que dans la version actuelle du formulaire KUDiR approuvé par le ministère des Finances de la Russie, cet indicateur n'est pas disponible).

Pour la méthode de distribution Revenu accepté (NU) L'assiette utilisée est le montant des revenus d'un entrepreneur individuel pris en compte pour déterminer l'assiette de l'impôt unique payé au titre du régime fiscal simplifié (indicateur Revenu de KUDiR) majorés des revenus attribués aux activités soumises à l'UTII (également déterminés selon la méthode de la trésorerie).

Le programme de comptabilité « 1C : Comptabilité 8 » version 3 a été créé pour le travail non seulement des organisations relevant du régime fiscal général, mais également des entrepreneurs individuels (ci-après dénommés entrepreneurs individuels) relevant du régime fiscal simplifié (ci-après dite fiscalité simplifiée). Après avoir acheté le programme, vous devez l'installer sur votre ordinateur, puis configurer la politique comptable et effectuer d'autres paramètres de comptabilité à l'aide d'un système de taxation simplifié. Voyons comment configurer facilement et facilement dans cet article.

Mise en place des politiques comptables du régime fiscal simplifié dans le programme 1C

Les paramètres de politique comptable sont les suivants :

- Activité principale ;

- La nature des activités de l’entrepreneur individuel ;

- Système fiscal.

Tous ces paramètres sont stockés dans le registre le plus important du programme 1C - il s'agit de la « Politique comptable des organisations », puisque les paramètres de ce registre déterminent la manière dont les transactions financières et commerciales seront reflétées dans les comptes comptables. Allez dans le menu principal dans la section « Principal », puis sélectionnez « Paramètres » et dans celui-ci « Politique comptable ».

- Actions ;

- Coût;

- Réserves ;

- Banque et caisse.

Sur l'onglet « STS », renseignez les informations suivantes :

- L'objet de l'imposition est fixé à « Revenus moins dépenses » ou « Revenus ». Lorsque vous sélectionnez « Revenus moins dépenses », un bloc s'ouvre pour remplir la « Procédure de comptabilisation des dépenses ». Dans lequel se trouvent des sections : coûts matériels ; les dépenses pour l'achat de biens; TVA en amont ; dépenses supplémentaires incluses dans le coût ; paiements douaniers. Certaines positions ont déjà été cochées, d'autres doivent être vérifiées ;

- Taux d'imposition, à l'heure actuelle pour l'objet d'imposition « Revenus moins dépenses », le taux est de quinze pour cent, « Revenus » le taux est de six pour cent ;

- La procédure de base pour refléter les avances de l'acheteur ;

- Si avant le régime fiscal simplifié le régime fiscal général était appliqué, il est alors nécessaire d'établir le signe et la date de transition vers le régime fiscal simplifié.

Dans l'onglet « Inventaire », renseignez les données suivantes :

- La méthode d'évaluation des stocks (stock) est au coût moyen ou FIFO, lors de leur cession (radiation) ;

- La méthode de valorisation des biens au détail est au coût d'acquisition ou au prix de vente.

Dans l'onglet « Coûts », renseignez les données suivantes :

- Le principal compte de comptabilité analytique est choisi dans la comptabilité, il peut s'agir du compte 26 « Frais généraux d'entreprise », du compte 44.01 « Frais de distribution dans les organisations exerçant des activités commerciales » ou du compte 44.02 « Frais de distribution dans les organisations exerçant des activités industrielles ou autres activités de production » ;

- Si l'entreprise exerce des activités de production, alors le type d'activité est indiqué (production ou exécution de travaux, prestation de services aux clients), les coûts sont pris en compte sur le compte 20 « Production principale » ;

Lorsque l'attribut « Exécution des travaux, prestation de services aux clients » est établi, un bloc est ouvert pour amortir les coûts encaissés au cours du mois calendaire sur le compte 20 (en prenant en compte uniquement les revenus des prestations de production, hors revenus de l'exécution des travaux ou prestation de services, en tenant compte des revenus provenant de l'exécution de travaux ou de prestations de services) ;

- Sur la comptabilisation des coûts indirects ;

- Selon les calculs du coût des produits semi-finis et comment les écarts par rapport au coût prévu sont pris en compte dans le bloc « Supplémentaire ».

Dans l'onglet « Réserves », un indicateur est activé si des réserves pour créances douteuses sont constituées en comptabilité (ci-après dénommées BU). Des réserves sont constituées uniquement pour les dettes en souffrance.

Dans l'onglet « Banque et caisse », un panneau est placé indiquant la nécessité d'utiliser le compte 57 « Virements en transit » lors du déplacement de fonds.

Vous pouvez imprimer ce document en cliquant sur le bouton « Imprimer » dans le programme 1C :

- Arrêté sur les politiques comptables ;

- Politique comptable pour la comptabilité ;

- Plan comptable fonctionnel ;

- Formes de documents primaires ;

- Registres comptables ;

- Politique de comptabilité fiscale ;

- Registres de comptabilité fiscale.

Un entrepreneur individuel opérant sous une fiscalité simplifiée peut enregistrer ses activités avec le paiement de l'Impôt Imputé Unifié (ci-après dénommé UTII). Dans ce cas, l'attribut « L'organisme est contribuable à l'impôt unique sur les revenus imputés (UTII) » est établi.

Un entrepreneur individuel opérant sous une fiscalité simplifiée peut enregistrer ses activités avec le paiement de l'Impôt Imputé Unifié (ci-après dénommé UTII). Dans ce cas, l'attribut « L'organisme est contribuable à l'impôt unique sur les revenus imputés (UTII) » est établi.

Après cela, vous devez remplir la section « Types d'activités » sur l'onglet « UTII ». En cliquant sur le bouton « Créer », les champs à remplir s'ouvrent :

- Organisation;

- Code d'activité ;

- Nom (type d'activité) ;

- Adresse - lieu d'activité (sélectionné dans l'annuaire KLADR - pays, code postal, ville, rue, maison, immeuble, appartement) ;

- OKTMO (Classificateur panrusse des territoires municipaux) ;

- Date d'inscription ;

- Date de désinscription ;

- Le bloc « Inspection des impôts », qui contient des informations sur l'administration fiscale ;

- Bloquer "Calcul des taxes".

Rapports dans le cadre d'une fiscalité simplifiée dans le programme 1C

Rapports dans le cadre d'une fiscalité simplifiée dans le programme 1C

Il y a peu de déclarations dans le cadre du régime fiscal simplifié. Dans le programme 1C, cette fonction est prévue dans la rubrique « Rapports », puis allez dans le bloc « STS » elle a deux positions :

- Déclaration selon le régime fiscal simplifié ;

- Livre des revenus et dépenses du régime fiscal simplifié.

Livre de comptabilité des revenus et dépenses (ci-après dénommé KUDiR) dans le programme de comptabilité 1C

Avant de remplir KUDiR, vous devez sélectionner :

- La période pendant laquelle il sera constitué ;

- Organisation.

Après cela, cliquez sur le bouton « Créer », et après avoir attendu un court instant, le livre terminé apparaîtra à l'écran.

S'il y a des sections vides (non remplies) dans le livre, elles peuvent alors être désactivées pour être générées dans le programme 1C et reflétées sur l'écran de l'ordinateur en accédant aux paramètres du rapport.

KUDiR diffère de celui qui le remplit en tant qu'entrepreneur individuel dont l'objet fiscal est « Revenus » ou l'objet fiscal « Revenus moins dépenses ». Le livre des revenus et dépenses doit être conservé pendant quatre ans à compter de la fin de la période fiscale (année).

A chaque période fiscale, un nouveau livre des revenus et dépenses est rempli. Si une entreprise comporte des divisions distinctes, elle est de toute façon gérée seule.

Le livre de comptabilité des revenus et dépenses comporte plusieurs sections :

- La première section présente quatre tableaux, chacun pour un trimestre de l'année d'imposition. La première colonne indique la numérotation. La deuxième colonne indique le numéro et la date du document principal (par exemple : ordres de paiement, ordres d'encaissement, etc.). La troisième colonne contient un bref résumé. Dans la quatrième colonne - le montant des revenus qui sera pris en compte lors du calcul de l'assiette fiscale lors du calcul de l'impôt. La cinquième colonne indique comment les subventions gouvernementales reçues sur le compte de l'entrepreneur individuel ont été dépensées ;

- La deuxième section présente les montants des dépenses sur les immobilisations et les immobilisations incorporelles ;

- La troisième section calcule le montant des pertes ;

- Dans la quatrième section, la première colonne indique une numérotation continue. Dans la deuxième colonne - la date, le nom du document et son numéro. La troisième colonne indique le numéro de l'année pour laquelle les montants des certificats d'incapacité de travail (cotisations d'assurance) ont été payés (versés). Les colonnes quatre à neuf reflètent les montants payés. Dans la dixième colonne - le montant total des dépenses reflétées.

Il faut savoir que les montants des ventes et des dépenses ne seront inclus dans KUDiR qu'après paiement des travaux, des services ou des biens.

Il faut rappeler que la procédure de lancement de la formation de KUDiR ne doit être effectuée qu'après « ».

Vous pouvez effectuer les réglages en cliquant sur le bouton « Afficher les paramètres ». Il est indiqué s'il faut ou non faire des décryptages dans le livre des revenus et dépenses.

Il est conseillé de faire le paramétrage « Produire des relevés de notes » dans le livre des revenus et dépenses pour détecter les erreurs dans le processus d'établissement du livre.

Vous pouvez imprimer un livre de ce magazine.

Il n'est pas nécessaire de soumettre le KUDiR au bureau des impôts. Mais il doit être à la disposition de l'entrepreneur individuel, numéroté, cousu et de préférence rempli correctement. Le Code des impôts de la Fédération de Russie prévoit une amende de 200 roubles pour un entrepreneur individuel pour l'absence de KUDiR et de 10 000 roubles pour une organisation.

Il est donc préférable de réaliser le KUDiR pour ne pas s'exposer à nouveau à des sanctions.

Déclaration selon le régime fiscal simplifié

Ce bloc renseigne également l'organisation et la période pour laquelle le reporting sera généré.

Après avoir sélectionné une organisation, un bloc s'ouvre à remplir - "Indicateurs de calcul de l'impôt". Vous pouvez calculer le montant de l'impôt à payer. En cliquant sur le bouton « Calculer la taxe », le programme effectuera automatiquement le calcul et indiquera le montant requis à payer. Si des erreurs sont détectées dans les documents, une fenêtre s'ouvrira pour les indiquer. Vous pouvez également facilement rapprocher les calculs avec le Service fédéral des impôts en cliquant sur le bouton « Demander un rapprochement avec le Service fédéral des impôts » dans le bloc « Rapprochement avec le Service fédéral des impôts ».

Après avoir sélectionné une organisation, un bloc s'ouvre à remplir - "Indicateurs de calcul de l'impôt". Vous pouvez calculer le montant de l'impôt à payer. En cliquant sur le bouton « Calculer la taxe », le programme effectuera automatiquement le calcul et indiquera le montant requis à payer. Si des erreurs sont détectées dans les documents, une fenêtre s'ouvrira pour les indiquer. Vous pouvez également facilement rapprocher les calculs avec le Service fédéral des impôts en cliquant sur le bouton « Demander un rapprochement avec le Service fédéral des impôts » dans le bloc « Rapprochement avec le Service fédéral des impôts ».

Très souvent, les comptables doivent ajouter un client supplémentaire au programme, mais peu d'entre eux savent comment ajouter une autre base de données dans 1C. Dans de tels cas, il est recommandé de ne pas essayer de résoudre le problème vous-même. Il est préférable de demander immédiatement l'aide qualifiée de spécialistes qui savent effectuer cette opération rapidement et correctement. Ils vous expliqueront également comment ajouter une base de données à 1C UNF. Vous pouvez obtenir une aide qualifiée en contactant la société Setby. Nos spécialistes connaissent bien le travail des programmes de comptabilité et répondront donc à toutes les questions des utilisateurs.

Comment ajouter une autre base de données dans 1C 8 ?

Il existe plusieurs façons d'ajouter des informations supplémentaires au programme. Ce n’est pas une tâche difficile que presque tous les comptables peuvent accomplir. Mais les méthodes de chargement des données peuvent différer en fonction de certains facteurs. Par exemple, vous pouvez généralement rajouter rapidement une base de données dans 1C à l'aide de l'outil interne approprié. Dans le même temps, l'inclusion d'un objet précédemment créé dans la liste s'effectue toujours sans problème ni erreur.

Mais s'il est nécessaire d'ajouter une nouvelle base de données, l'utilisateur peut alors rencontrer des difficultés. Par conséquent, si vous cherchez un moyen d'ajouter une base de données standard à 1C, il est conseillé de consulter des spécialistes. Par exemple, vous pouvez bénéficier d'une assistance qualifiée des employés de notre société « Setby ». Le support technique est disponible 24h/24 et 7j/7, alors contactez-nous à tout moment.

Comment ajouter un entrepreneur individuel à la base de données 1C ?

De nombreux comptables s'occupent de la tenue de la documentation non pas d'une entreprise, mais de plusieurs à la fois. Par conséquent, pour la commodité de leur travail, dans 1C, il est possible d'ajouter de nouveaux entrepreneurs individuels à la base de données. Cependant, les spécialistes ont des difficultés à saisir les données après la mise à jour du programme. Beaucoup, après l'introduction de la version 8.3, ne peuvent pas

ajouter une autre entreprise à la base de données 1C.

Cette fonctionnalité n’a pas été supprimée, mais simplement légèrement transformée. Désormais, pour ajouter un autre entrepreneur individuel à la base de données, vous devez ouvrir l'onglet « Entreprise ». Dans la liste qui apparaît, sélectionnez « Organisations ». Ensuite, dans la section « Actions », ajoutez un autre utilisateur à la base d'informations 1C. En règle générale, l’opération est rapide et ne pose aucune difficulté.

Aide à l'ajout d'une base de données à 1C

Presque tous les comptables rencontrent de temps en temps des difficultés à travailler dans le programme. Il est donc très important qu'un spécialiste puisse recevoir rapidement une aide ou des conseils qualifiés. Notre société fournit de tels services. Les spécialistes Setbi savent comment ajouter un élément à la base de données 1C et comment ajouter un nouvel entrepreneur individuel.

Nous employons uniquement des spécialistes hautement qualifiés possédant une vaste expérience. Ils sont prêts à vous aider à résoudre tout problème, dysfonctionnement ou problème technique. Ils savent comment ajouter KLADR à la base de données 1C et partageront ces informations utiles avec vous.

Les contreparties dans 1C 8.3 sont l'un des répertoires les plus importants dans presque toutes les configurations standard. Cet annuaire stocke des informations sur les clients, les fournisseurs et d'autres entités juridiques et personnes physiques avec lesquelles l'entreprise interagit. Voyons comment créer un nouveau fournisseur ou acheteur et vérifier la contrepartie à l'aide du numéro d'identification fiscale (TIN).

Voyons comment ajouter une contrepartie dans 1C. Pour tenir à jour une liste des contreparties en 1C : Comptabilité, il existe un ouvrage de référence « Contreparties ». Où puis-je le trouver ? Vous devez vous rendre dans le menu « Annuaires », rubrique « Contreparties ».

La fenêtre du formulaire de liste de répertoires s'ouvrira. Pour ajouter un nouvel élément de répertoire, cliquez sur le bouton « Créer » ou sur la touche « Insérer » du clavier. Un formulaire s'ouvrira pour remplir et modifier les données de la contrepartie.

Travailler avec le service Contrepartie 1C

Actuellement, le système a la capacité d'obtenir des données sur la contrepartie et de les vérifier par son NIF ou son nom. Les dossiers sur les contreparties sont extraits des registres d'État du Registre d'État unifié des personnes morales/Registre d'État unifié des entrepreneurs individuels.

Important! Le service 1C Counterparty est disponible uniquement pour ceux qui ont souscrit au support informatique (ITS) et ont payé pour accéder au service 1C Counterparty.

Le coût du service d'entrepreneur 1C est de 4 800 roubles pour 12 mois (vous pouvez commander le service auprès de). Si, pour une raison quelconque, votre organisation ne s'abonne pas à ITS, les données peuvent être saisies manuellement. Considérons les deux options.

Si vous êtes abonné, mais que le service Contrepartie 1C ne fonctionne pas ou affiche des erreurs pendant le fonctionnement, vous devez vérifier vos paramètres de connexion. Pour cela, allez dans le menu « Administration », rubrique « Connexion du support Internet ». Cliquez sur le bouton « Connecter le support Internet ». Dans la fenêtre qui s'ouvre, saisissez votre nom d'utilisateur et votre mot de passe pour vous connecter. Cliquez sur le bouton «Connexion», et si tout est saisi correctement, vous serez connecté à 1C Counterparty.

Nous entrons le NIF, cliquons sur le bouton « Remplir » et, si la contrepartie avec le même NIF est trouvée dans le registre d'État, nous obtenons l'image suivante :

Obtenez 267 leçons vidéo sur 1C gratuitement :

Comme vous pouvez le constater, tous les champs nécessaires avec les données de la contrepartie sont remplis, il ne reste plus qu'à les vérifier au cas où et à cliquer sur le bouton « Enregistrer ». La ligne « Adresse et téléphone » s'ouvre si vous cliquez sur le bouton « > ». Nous verrons ici les adresses légales, réelles et postales. S'ils correspondent, vous pouvez cocher les cases appropriées.

Si vous ne disposez pas de support Internet, vous pouvez saisir manuellement les coordonnées de la contrepartie, à partir du champ « Type de contrepartie ».

Si vous devez créer une contrepartie étrangère en 1C, vous devez déterminer le pays de son enregistrement. Après cela, des champs deviendront disponibles pour que le fournisseur ou l'acheteur étranger puisse les remplir. Cela masquera les champs TIN et point de contrôle.

Saisie d'un accord ou d'un compte bancaire d'une contrepartie

Dans 1C : Comptabilité 8.3, presque tous les documents nécessitent une indication de l'accord de contrepartie, vous devez donc immédiatement créer au moins un accord. Chaque contrepartie de notre organisation peut être un acheteur, un fournisseur, un donneur d'ordre, etc. Par conséquent, les contrats sont divisés en types. Les types de contrats suivants sont proposés :

- Avec le fournisseur.

- Avec l'acheteur.

- Avec l'engagement.

- Avec un commissionnaire.

- Autre.

Supposons que les transactions avec cette contrepartie seront principalement réalisées sur la vente de biens et de services. Suivez ensuite le lien « Accords » vers la liste des accords et ajoutez-y un nouvel accord. Type d'accord – « Avec l'acheteur », nom « Accord principal ». Désormais, par exemple, dans le document « », lorsque vous sélectionnerez cette contrepartie, le champ « Accord » sera renseigné automatiquement.

Pour effectuer des opérations bancaires, vous devez ajouter un ou plusieurs comptes bancaires à votre contrepartie (lien « Comptes bancaires »).

La contrepartie est prête à travailler.

Regardez également notre vidéo sur le remplissage du répertoire « Contreparties » :

Vérification du NIF de la contrepartie

Il n'est pas obligatoire de remplir le champ TIN, mais s'il est rempli, le système vérifiera d'abord l'exactitude de la valeur saisie. Le NIF doit être conforme au format introduit par le Service fédéral des impôts de la Fédération de Russie. Le contrôle des contreparties à l’aide de numéros d’identification fiscale et de points de contrôle est devenu particulièrement pertinent après les récentes innovations en matière de déclarations de TVA.

De plus, lors de la saisie du TIN, l'unicité de la valeur dans l'annuaire est vérifiée. Si une contrepartie avec le même TIN existe déjà dans l'annuaire, un avertissement sera émis. Ceci est nécessaire pour éviter les éléments en double.

Ces contrôles ne nécessitent pas de connexion permanente à Internet.

À l'heure actuelle, dans les dernières versions de 1C : Comptabilité, un nouveau service est apparu permettant de vérifier le NIF directement dans la base de données du Service fédéral des impôts. Ce service nécessite une connexion Internet permanente. Il est activé dans le menu « Administration », rubrique « Support et maintenance ».

Cochez la case appropriée et cliquez sur le bouton « Vérifier l'accès au service Web ».

Si l'accès réussit, le programme nous en informera.

Depuis longtemps, personne ne fait la comptabilité manuellement. Des programmes spéciaux sont utilisés pour la comptabilité dans les entreprises. La société 1C a acquis une grande popularité dans ce domaine, produisant de nombreuses solutions standard visant à effectuer diverses tâches comptables d'une entreprise.

Dans cet article, nous parlerons de l'une des configurations les plus courantes de 1C Comptabilité, à savoir 1C version 8.2. Le programme 1C 8.2 se compose d'une plate-forme et d'une configuration : la plate-forme a différentes versions (pour les besoins de cet article, la version 8.2 de la plate-forme est prise en compte) et la configuration comptable.

1C:Entreprise 8 et 1C:Comptabilité 2.0

La comptabilité 8.2 est utilisée pour tenir une comptabilité automatisée et une comptabilité fiscale dans les entreprises de diverses formes de propriété, y compris la préparation de rapports réglementés conformément aux exigences de la législation de la Fédération de Russie.

Comptabilité 8.2 a plusieurs éditions. Pour la version 8.2 de la plateforme, la configuration avec le numéro de révision 2.0* est utilisée. Il existait une édition encore antérieure de Comptabilité 1.6 et une édition ultérieure de 1C Comptabilité - 3.0. L'édition 3.0 est utilisée avec la version 8.3 de la plateforme plus moderne. Pour passer à la version 3.0, vous devrez également mettre à jour la plateforme. Parce que Cet article est consacré à la plateforme 8.2, nous parlerons ensuite des capacités de Accounting 8.2 dans la version 2.0.

*L'édition est une mise à jour de la configuration 1C, qui est associée à l'amélioration du système en termes technologiques et fonctionnels, en raison de nouvelles exigences légales, du développement des technologies informatiques ou de l'émergence de nouvelles méthodes commerciales.

Comptabilité 8 contient tous les ouvrages de référence nécessaires au travail d'un comptable : documents, rapports, et permet également de collecter des rapports sans aucun effort supplémentaire, ce qui optimise et en même temps simplifie le travail d'un comptable. Parallèlement, la version 8.2 permet de conserver simultanément les enregistrements de plusieurs organisations.

Caractéristiques de la comptabilité en version 8.2

Comptabilisation de plusieurs organisations dans une seule base de données

Contrairement à la version 7, dans 1C : Comptabilité 8, la comptabilité est devenue plus pratique du fait que la comptabilité de différentes organisations peut être conservée dans une seule base de données à l'aide de répertoires communs, ce qui simplifie certainement le processus* lorsque les entreprises sont interconnectées. Grâce à cette fonctionnalité, 1C : Comptabilité 8, à savoir la version en cours de révision - 8.2, est demandée aussi bien dans les petites entreprises que dans les exploitations.

*Cette fonction est utile non seulement pour les comptables, mais aussi pour les chefs d'entreprise, car ils peuvent recevoir des rapports pour toutes les organisations à la fois à partir d'une seule base de données.

Comptabilisation des différents systèmes fiscaux

1C : Comptabilité 8.2 vous permet de tenir des registres pour les organisations avec différents régimes fiscaux :

- Régime fiscal général. La version 2.0 utilise un plan comptable unifié pour la comptabilité et la comptabilité fiscale* ;

- Fiscalité simplifiée (STS). Des dispositions sont prises pour tenir des registres des revenus et des dépenses ;

- Impôt unifié sur les revenus imputés (UTII). Permet de maintenir des revenus et dépenses distincts pour les activités de l'entreprise sous le régime général et celles relevant de l'UTII.

Lors de l'utilisation de la version 8.2, il n'est pas nécessaire d'acheter plusieurs configurations de comptabilité pour les organisations et les entrepreneurs individuels qui utilisent des modes spéciaux.

*Dans la version 1.6, deux plans comptables distincts étaient utilisés pour la comptabilité et la comptabilité fiscale.

Options de personnalisation

Examinons les principales fonctionnalités disponibles dans Accounting 8.2 et distinguons-les des autres versions et éditions.

Pour simplifier le travail en 1C : Comptabilité 8, il existe différents assistants :

Lancé à l'ouverture du programme, il facilite le remplissage et la vérification des paramètres de base du programme, des répertoires et la saisie des soldes initiaux. De plus, à l'aide de cet assistant, vous pouvez transférer des données des versions précédentes de 1C.

Souvent, les comptables sont confrontés à un problème lorsqu'ils doivent effectuer une certaine écriture, mais ils ne savent pas quel document doit être utilisé pour refléter cela dans le système 1C. A cet effet, dans la version 8.2 un nouvel assistant est apparu, appelé « Invoice Correspondence Directory ». De plus, cet ouvrage de référence vous aidera à savoir quel document refléter l'affichage nécessaire, où le trouver dans le programme et quel type d'opération choisir.

Les comptables qui viennent tout juste de s'habituer au programme de comptabilité 1C apprécieront particulièrement un tel assistant. Cet assistant se trouve dans la section Opérations – Correspondance compte.

L'assistant ressemble à ceci :

Cet assistant est conçu pour simplifier le travail lors de la saisie des données sur les nouveaux employés dans 1C, en calculant les salaires et les impôts les concernant. L'assistant se trouve dans la section Salaire - Assistant Paie.

Modifications du plan comptable et reflet des transactions dans la version 8.2

1C : Comptabilité 8 comprend un plan comptable approuvé par arrêté du ministère des Finances de la Fédération de Russie. Les utilisateurs peuvent désormais ajouter indépendamment de nouveaux comptes, de nouveaux sous-comptes et des sections de comptabilité analytique. Pour tenir la comptabilité fiscale, un plan comptable unifié est utilisé et le signe de tenue de la comptabilité fiscale est défini dans le plan comptable dans l'attribut « Taxe ».

Les paramètres de chaque compte sont visibles en ouvrant le compte en double-cliquant sur la souris :

La comptabilité en Comptabilité 8.2 est effectuée « à partir du document » - cela signifie que les documents reflétant une transaction commerciale sont saisis dans le programme et, une fois exécutés, le document génère des transactions et des inscriptions dans les registres. La comptabilité fiscale est effectuée automatiquement lorsque les documents sont reflétés dans 1C. Une transaction reflète désormais les données comptables et fiscales. Vous pouvez visualiser les transactions et les entrées dans les registres générées par un document spécifique en cliquant sur le bouton « Résultat de la comptabilisation du document ».

La capture d'écran montre que les données comptables et fiscales sont dans une seule entrée, les montants sont indiqués dans différentes colonnes.

Dans le programme Comptabilité 8.2, la plupart des opérations commerciales sont automatisées. Cependant, dans la pratique, il arrive qu'un comptable soit confronté à la nécessité de refléter une transaction non standard, pour laquelle 1C Comptabilité ne fournit pas de document séparé. Pour ce faire, le programme dispose d'une saisie manuelle des données, où la comptabilisation est saisie directement. La version précédente du programme nécessitait la saisie de deux documents. Un document effectuait des écritures comptables, un autre document effectuait des inscriptions dans les registres*. Dans la version examinée, ce travail est simplifié du fait que désormais la saisie des transactions et des données dans les registres s'effectue dans un seul document, appelé « Opérations saisies manuellement ».

*A cet effet, le document « Ajustement des inscriptions au registre » a été utilisé.

Procédure de clôture d'une période

Lors de la clôture d'une période, de nombreuses opérations de routine sont effectuées dans un ordre strictement défini. Le programme de clôture d'une période dispose d'un assistant appelé « Clôture du mois ». Vous pouvez le retrouver dans Opérations – Traitement – Clôture Mois. Avant la clôture, l'ordre de saisie des pièces est vérifié par ordre chronologique afin de détecter les pièces qui pourraient avoir été saisies de manière antidatée, ce qui pourrait entraîner des erreurs comptables. Pour restaurer la séquence, vous devez utiliser le bouton « Repost Documents ». Une fois terminé, le contrôle de la séquence sera rétabli et il sera possible de commencer à clôturer la période. Si le comptable est sûr que les documents saisis rétroactivement n'entraîneront pas d'erreurs comptables, vous ne pouvez pas republier les documents, mais cliquez sur le bouton « Modifier le jour de référence », reconnaissant ainsi la séquence de documents existante comme correcte.

Dans la version 8.2. édition 2.0, lors de la clôture d'une période, vous pouvez voir clairement quelle opération a été effectuée avec succès, dans laquelle des erreurs se sont produites et quelle opération n'a pas été effectuée du tout. Pour plus de clarté, tout est mis en évidence dans une couleur différente.

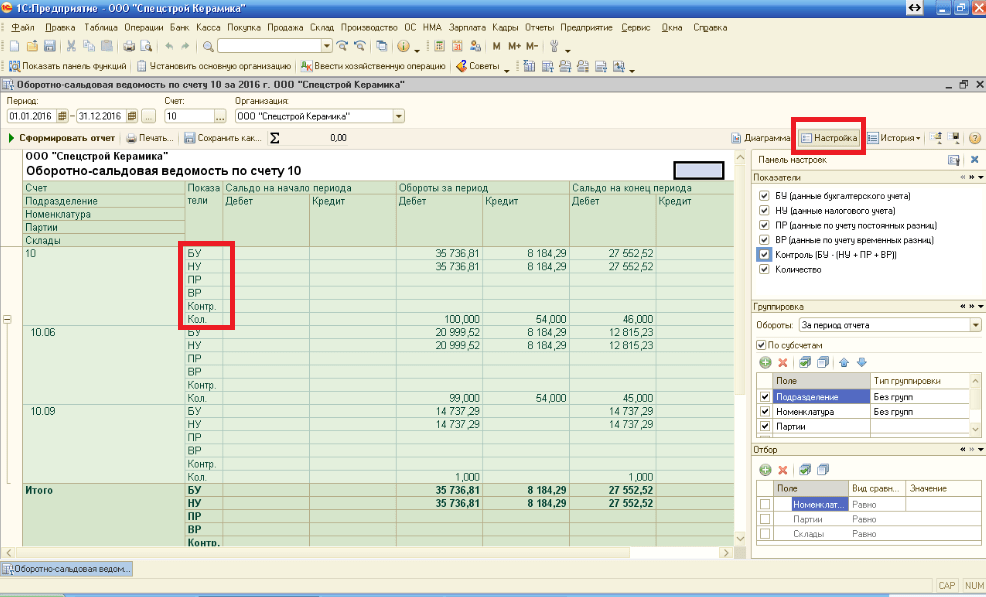

Vous pouvez utiliser des rapports pour rapprocher, comparer et organiser les données. Dans la version 8.2, le rapprochement des données entre la comptabilité et la comptabilité fiscale est devenu plus pratique, puisque la version du programme évoquée dans cet article vous permet de les voir dans un seul rapport. De nouvelles opportunités sont apparues dans les rapports pour regrouper, trier, personnaliser et sélectionner les données.

Par exemple, nous utiliserons le rapport « Bilan du compte ». Lors de la configuration d'un rapport, vous pouvez utiliser le panneau des paramètres (ouvert en cliquant sur le bouton « paramètres » sur le côté droit du rapport) pour afficher dans le rapport les données nécessaires sur la comptabilité fiscale et le contrôle de l'égalité comptable avec la comptabilité fiscale.

Nous avons examiné les fonctionnalités de base et certaines fonctionnalités du programme Accounting 8.2 dans l'édition 2.0, qui permettent de simplifier et d'améliorer la comptabilité dans n'importe quelle entreprise, mais c'est loin d'être une liste exhaustive de toutes les capacités du programme.